The number of 3G subscriber connections in India are expected to triple within four years, to reach 400 million, representing almost one in three phones. This is the main finding of a new study by the UK-based Wireless Intelligence (India 3G rollout (forecasts and market shares 2011 – 2015). Indian operators spent a combined $15 billion in acquiring WCDMA 3G spectrum at auctions last year and are forecast to jointly invest a further $2.5 billion in building the new networks and rolling out 3G services in 2011.

Seven private operators acquired 3G spectrum last year in addition to the two state-owned operators (BSNL and MTNL) that had already been awarded 3G airwaves ahead of the private auctions. The study suggests that over 80 percent of 3G connections will be based on WCDMA ( the 3G path for GSM) in five years, with the remaining 20 percent on CDMA-based 3G networks.

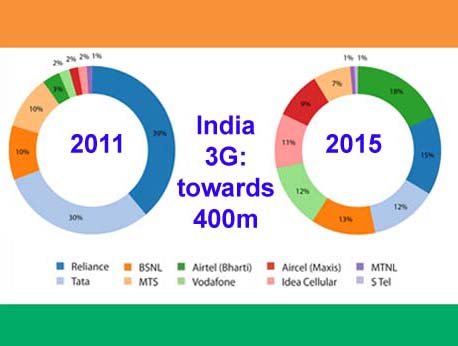

Reliance Communications and Tata Teleservices Ltd (TTSL) which both offered 3G CDMA for a decade are now also in the GSM space and in the process of migrating to GSM/WCDMA. In fact were the first two private operators to launch services using new WCDMA spectrum in late 2010. Reliance and TTSL are set to command 3G market shares of 39 percent and 30 percent, respectively, this year, according to the study.

This yearhas already seen a succession of rival launches – including Bharti (in January), Aircel (February) and Vodafone (March) – and Wireless Intelligence forecasts that all new WCDMA-based operators will have launched services by June 2011. This means that, by 2015, 3G market shares will more closely resemble the overall national picture: Bharti – India's largest operator - is forecast to command the largest 3G share (18 percent), followed by Reliance (15 percent) and BSNL (13 percent).

"Competition in the Indian 3G space is likely to be intense as most operators have set ambitious targets," says Joss Gillet, Senior Analyst at Wireless Intelligence and author of the report. "Market share growth clearly depends on how fast operators can deploy 3G networks in their respective licensed areas, and how rapidly they can address demand in rural areas. Nevertheless, 3G will remain a niche market for some time in India, and 2.1GHz networks will initially be mainly used to improve voice quality and reduce congestion in existing 2G networks."

Rise of the secondary regions

The study notes that India's Circle A and Circle B service areas will account for 75 percent of the country's 3G connections by 2015. Even though initial 3G rollouts are concentrated in the so-called metro areas (Mumbai, Delhi, Kolkata) they will soon be outstripped by fast-growing demand for 3G in more populous regions such as Punjab, Bihar, Andhra Pradesh and Haryana, the report says. But the situation is complicated by the fact that no 3G operator is able to offer a nationwide service, which will require network sharing and roaming between operators. Pricing 3G services appropriately in a market where around 200 million prospective users live on less than Rs 100, a day is also set to be a major challenge.

"Indian operators are betting on 3G services to stabilise Average Revenue Per User and increase non-voice revenues to around the 30 percent mark in the coming years," adds Gillet. "Even though we do not anticipate a price war in the 3G space, profitability will take time due to the high investments required and the current need for additional spectrum. While network-sharing deals will help speed-up the adoption of 3G services and increase economies of scale, it is clear that device availability and affordability will have a more immediate impact on demand in such a price sensitive market dominated by prepaid users."

India 3G operator market share estimates in 2011 & 2015: Bharti Airtel 3% 18%

Reliance Comms 39% 15%

BSNL 10% 13%

Vodafone Essar 2% 13%

Tata Teleservices 30% 12%

IDEA Cellular 2% 11%

Aircel 2% 9%

MTS 10% 7%

MTNL 1% 1%

S-Tel 1% 1%

( source: Wireless Intelligence www.wirelessintelligence.com March 2011)

March 4 2011